Beyond the Numbers: How to Secure a Mortgage When Your Credit Score is Less Than Perfect

Let me tell you something I’ve learned over my years navigating the real estate trenches: a three-digit number shouldn’t dictate your family’s future.

If I had a dollar for every time a hard-working buyer sat across from me, thoroughly convinced their dream of homeownership was dead because of a bruised credit score, I’d have retired a long time ago. As real estate professionals, we are conditioned to worship the 800 FICO score, but here is the unvarnished truth: you do not need pristine credit to buy a house.

My experience has taught me that the mortgage industry isn’t just about algorithms; it’s about risk management. If you can prove to a lender that you are a safe bet, you can get the keys.

Here is my personal, battle-tested playbook for securing a mortgage when your credit score is lower than you’d like.

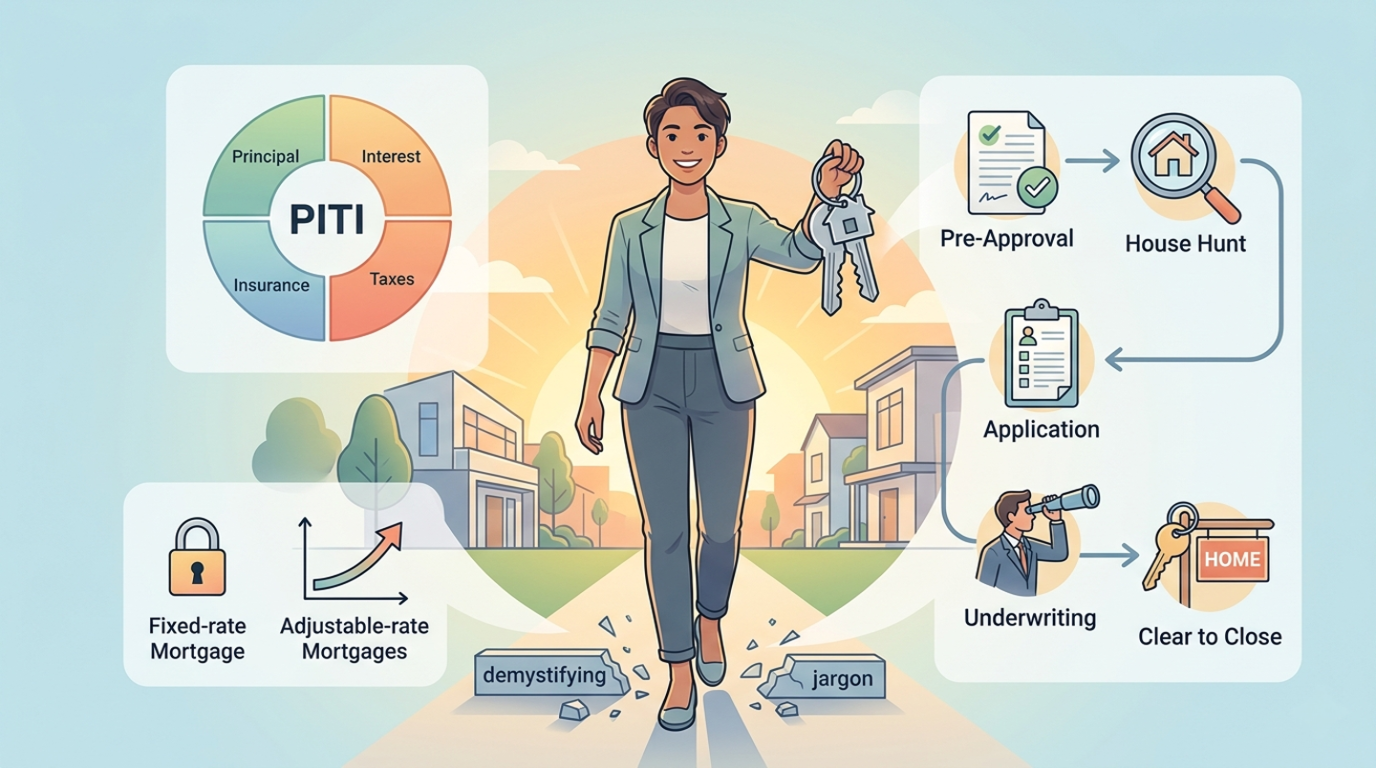

1. Stop Guessing and Get the Real Numbers

The very first thing I tell my clients is to stop looking at consumer credit apps. The score you see on your smartphone is usually a VantageScore. Mortgage lenders don’t care about that number; they use specific FICO scoring models (typically FICO 2, 4, and 5).

Often, I’ve seen buyers panic over a consumer score of 590, only to pull their actual mortgage credit report and find out they are sitting at a 620. Before you assume you can’t get a loan, speak to a mortgage broker and have them pull your actual tri-merge mortgage credit report. You need to know exactly where the baseline is before you can strategize.

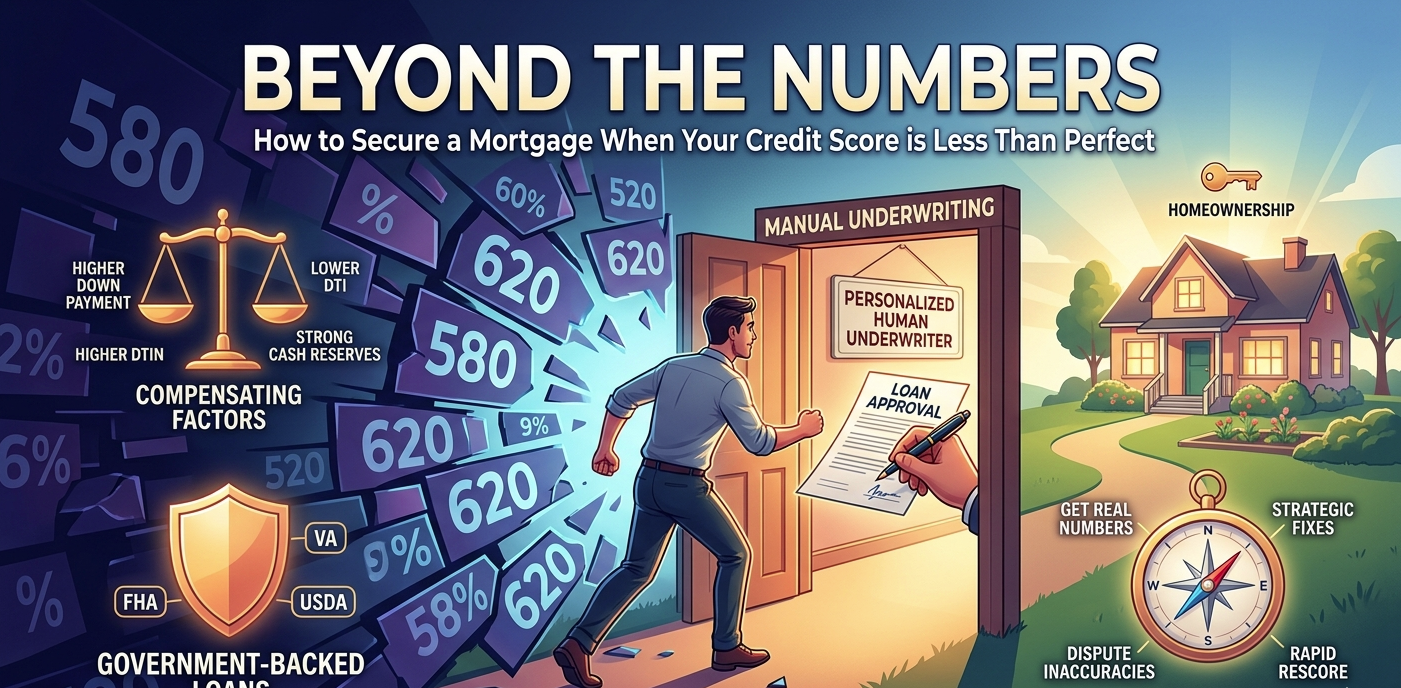

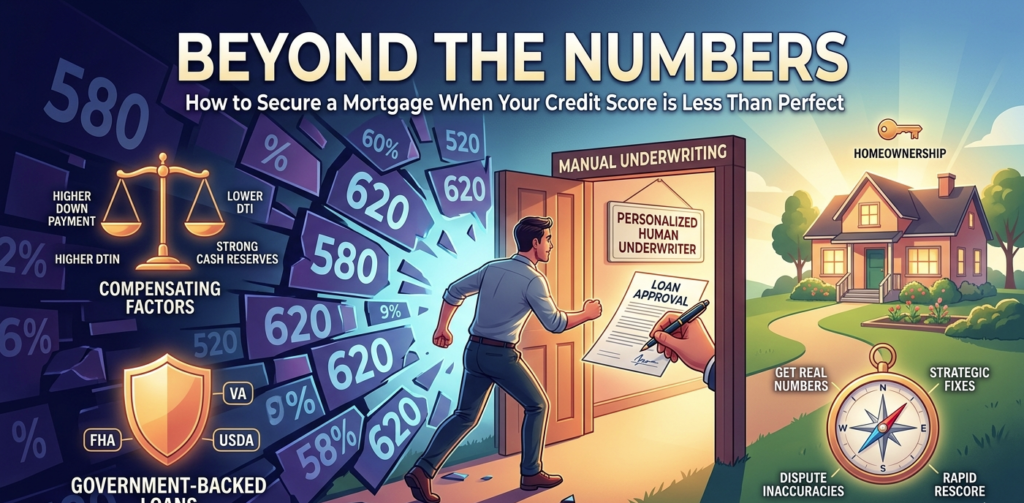

2. Leverage Government-Backed Loans

If your score has taken a hit, conventional loans (backed by Fannie Mae and Freddie Mac) are going to be an uphill battle. But government-backed loans were designed exactly for this scenario.

- FHA Loans: This is the bedrock of second chances. You can qualify for an FHA loan with a credit score as low as 580 while only putting down 3.5%. If your score is between 500 and 579, you can still get an FHA loan, provided you can bring a 10% down payment to the table.

- VA Loans: If you are a veteran or active-duty military, VA loans technically have no minimum credit score requirement set by the government, though most lenders look for a 580-620.

- USDA Loans: If you are willing to buy in a designated rural or suburban area, USDA loans offer zero-down-payment options with very flexible credit thresholds.

3. Bring “Compensating Factors” to the Table

In my practice, I always emphasize the concept of a balanced scale. If one side of your financial profile is weak (your credit score), you must weigh down the other side with “compensating factors.” Lenders want to see that you are offsetting their risk.

How do you do this?

- Lower your Debt-to-Income (DTI) ratio: Pay off your car or wipe out a lingering personal loan before applying.

- Save a larger down payment: If you can bring 10% or 15% instead of 3.5%, lenders are much more forgiving of past credit mistakes.

- Show strong cash reserves: Having three to six months of mortgage payments sitting untouched in a savings account proves you have a safety net.

4. Seek Out Manual Underwriting

When you apply for a mortgage, your file is run through an Automated Underwriting System (AUS). If your credit score is low, the computer will often kick back an automatic denial.

Don’t take a computer’s “no” as the final answer. You need to find a lender who does manual underwriting. This means a living, breathing human being will sit down, look at your file, and listen to your story. If your low credit score was due to an isolated medical emergency, a divorce, or a temporary job loss—but you have a flawless 12-month history of paying rent and utilities on time—a manual underwriter has the power to approve your loan.

5. Execute Strategic, Rapid Credit Fixes

Sometimes, you are only 10 to 15 points away from a better interest rate or a loan approval. Before you submit your final application, look for quick wins:

- Pay down revolving debt: Credit utilization accounts for 30% of your score. Paying your credit card balances down to below 10% of their limit can trigger a rapid score increase in less than 30 days.

- Dispute inaccuracies: I’ve seen clients dragged down by collections that were actually paid off years ago. Force the credit bureaus to remove erroneous marks.

- Ask for a Rapid Rescore: If you pay off a debt, your lender can request a “rapid rescore” to update your credit profile in a matter of days rather than waiting for the next monthly billing cycle.

Conclusion

Securing a mortgage with a low credit score is entirely possible, but it requires strategy, patience, and the right team around you. Don’t let past financial mistakes paralyze your future wealth-building.

Take a deep breath, pull your actual mortgage credit report, explore FHA options, and start building your case with compensating factors. Homeownership isn’t an exclusive club reserved only for those with perfect financial pasts—it is attainable for anyone willing to put in the work.

— Olivia Borges