From Renter to Owner: What Is a Mortgage and How Does It Actually Work?

If there is one moment I see repeated constantly in my real estate career, it’s the “deer in the headlights” look that washes over a first-time buyer’s face the second we start talking about financing.

Buying a home is incredibly exciting. You are dreaming of backyard barbecues, painting the walls whatever color you choose, and building long-term wealth. But before you get the keys, you have to cross the bridge of financing. For most people, that means getting a mortgage.

Over my years in this industry, I’ve sat across the table from countless individuals who feel completely overwhelmed by the financial jargon. My philosophy is simple: an educated buyer is an empowered buyer. Let’s strip away the complicated terminology and break down exactly what a mortgage is and how it works.

What Exactly Is a Mortgage?

At its absolute core, a mortgage is simply a loan used to purchase real estate.

Because homes are incredibly expensive, very few people have the cash on hand to buy them outright. A bank or mortgage lender steps in to provide the bulk of the money. In exchange, you agree to pay them back over a set period of years, plus interest.

Here is the key differentiator between a mortgage and a personal loan: collateral. The home itself secures the loan. If you stop making your payments, the lender has the legal right to take possession of the property (a process known as foreclosure) to recoup their money.

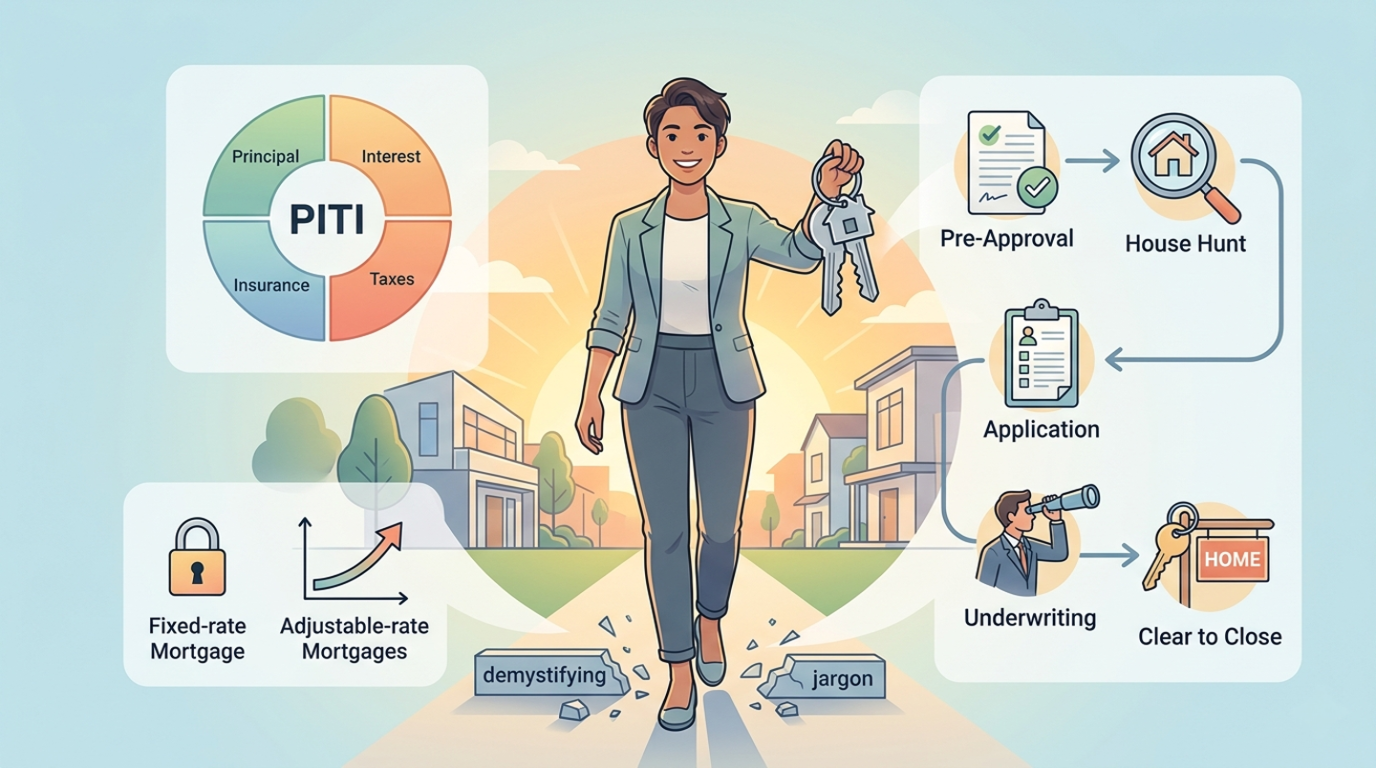

The Anatomy of Your Monthly Payment (PITI)

When my clients ask me, “Randy, what am I actually paying for every month?”, I introduce them to a real estate acronym: PITI. Understanding this is critical to understanding your true purchasing power.

- Principal: This is the money going directly toward paying down the actual balance of the loan. In the early years of your mortgage, this portion is small.

- Interest: This is the cost of borrowing the lender’s money. In the beginning, the majority of your monthly payment goes toward interest. Over time, as your loan balance decreases, the ratio flips, and you pay more toward the principal.

- Taxes: Most lenders will collect a portion of your annual property taxes every month and hold them in an “escrow” account, paying the tax bill on your behalf when it’s due.

- Insurance: Just like taxes, lenders usually collect your homeowner’s insurance premiums monthly. Furthermore, if you put down less than 20% on the home, you will likely be paying for Private Mortgage Insurance (PMI), which protects the lender if you default.

How the Process Actually Works

In my experience, anxiety comes from the unknown. Here is the standard timeline of how a mortgage works in the real world:

1. The Pre-Approval

Before we ever step foot in an open house, you need a pre-approval. A lender will look at your income, debts, and credit score, and issue a letter stating exactly how much money they are willing to lend you. This tells sellers you are a serious, qualified buyer.

2. The Hunt and The Offer

Once we know your budget, we find the perfect home and negotiate the deal. Once the seller accepts your offer, you are officially “under contract.”

3. Underwriting (The Deep Dive)

This is where the lender puts your financial life under a microscope. Their underwriters will verify your bank statements, tax returns, and employment status. During this time, they will also order a home appraisal to ensure the property is actually worth the amount you are paying for it.

4. The Closing Table

Once the underwriter gives the “Clear to Close,” we meet at the closing table. You sign a mountain of paperwork, the lender wires the funds to the seller, and you walk away with the keys to your new home.

Choosing the Right Loan for You

Not all mortgages are created equal. The type of loan you choose dictates your financial future for the next few decades.

- Fixed-Rate Mortgage: The interest rate stays exactly the same for the entire life of the loan (usually 15 or 30 years). I highly recommend this for most buyers because it offers predictable, stable monthly payments.

- Adjustable-Rate Mortgage (ARM): The interest rate is fixed for a short initial period (like 5 or 7 years) and then adjusts annually based on the broader market. These can be risky if rates spike, but useful if you plan to move before the initial period ends.

- Loan Programs: Depending on your situation, you might opt for a Conventional loan (standard), an FHA loan (great for lower credit scores and smaller down payments), or a VA loan (exceptional benefits for military veterans).

Conclusion: Don’t Let the Process Intimidate You

A mortgage is arguably the largest financial commitment you will ever make, but it shouldn’t be a source of fear. It is simply a financial tool, a stepping stone that allows you to transition from renting to owning, and from paying someone else’s mortgage to building your own equity.

If you surround yourself with experienced professionals, from a sharp real estate agent to a communicative mortgage broker, you will find that the process is highly manageable. Take it one step at a time, stay within your comfortable budget, and soon enough, you’ll be holding the keys to your future.

Here’s to your journey toward homeownership.

— Olivia Borges